SPECULATIVE RISK & PURE RISK

- Chegan SRM

- Feb 16, 2021

- 3 min read

Updated: Feb 12, 2023

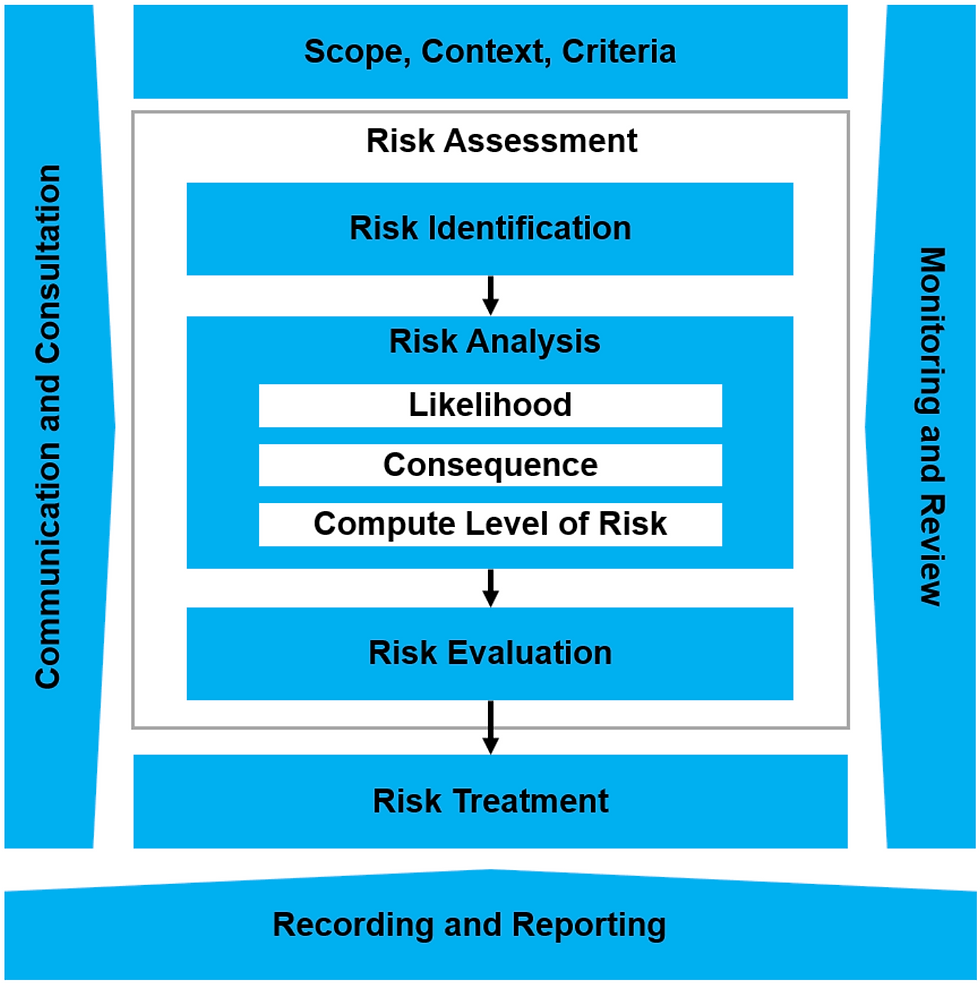

Risk is associated with the unwanted outcome of something harmful or damaging that can occur if the threat is not eliminated or contained.

The social context in which decision-making takes place will also affect a person’s judgment on the likelihood of risk. People who belong to a group or organization are likely to assimilate their own views to correspond to those of the majority irrespective of how they would reason in an isolated scenario where they weigh risks using a rational, logical reasoning process. Social psychologists coined this phenomenon “groupthink” and it’s been used to explain poor decision-making even at the highest levels of politics. A classic example of “groupthink” influencing decision-making is the failed attempt to overthrow Fidel Castro in the 1961 Bay of Pigs invasion fiasco.

Levels of risk are categorized into two types: speculative risk and pure risk.

Speculative risk refers to a perceived threat that can result in a loss or gain where the outcome could be either favorable or unfavorable (e.g. buying stock/shares, starting a new business, or releasing a new product). Since the threat may or may not materialize, managing speculative risks requires a proactive approach of identifying potential hazards. However, a biased view based on past history or social context may affect sound judgment in the decision-making process. For example, a recent victim of car theft is likely to perceive the risk of theft as higher than the likelihood of their car being broken into. Another person who parks frequently in the same parking lot and who has never had their car broken into or stolen may perceive the risk of car theft and burglary as minimal or negligible.

Although speculative risk can motivate those involved in the management process to think proactively about the potential of risk, it’s insufficient as a risk management strategy because it’s subjective and susceptible to individual and social biases. In many circumstances, the probability or likelihood of an occurrence cannot be determined because it is uncertain that an incident will ever take place.

Pure risk is defined as loss being the only outcome of a situation. Some examples include fires, natural disasters, burglary and computer hacking. Pure risks can be divided into three different categories: personal, property, and liability. There are no measurable benefits when it comes to pure risk. Instead, there are two possibilities: complete loss or no loss at all. In many cases of pure risk are insurable. An individual cannot control any type of pure risk and it can only result in loss with no possible gain. The most common method of dealing with pure risk is to transfer it to an insurance company by purchasing an insurance policy.

Are you looking for a way to manage the risks associated with your business?

Our risk management services can help you identify potential risks and take proactive steps to mitigate them. We specialize in both speculative and pure risk, so you can rest assured that no matter what type of risk you are facing, we have you covered. Our services provide a comprehensive approach to risk management, including assessing the likelihood of an event occurring and determining the best way to prevent or mitigate it. We also provide advice on how to transfer pure risks to an insurance company, making sure that no matter the outcome, you are protected. Contact us today to learn more about our risk management services!